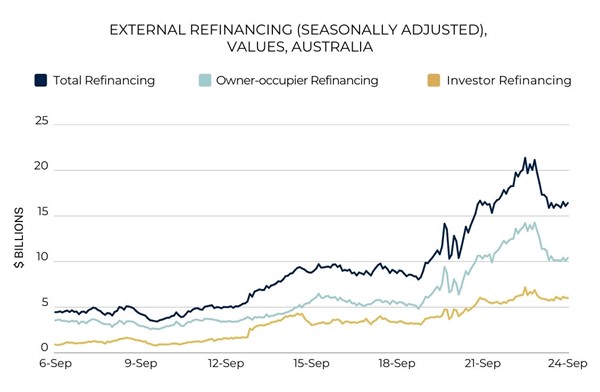

New year, new loan? Five signs it’s time to refinance

One of the biggest home loan mistakes you can make is to ‘set and forget’ your mortgage for 30 years, because as the market shifts and your financial situation changes, there’s a good chance your mortgage will no longer be as competitive or suitable.

With that in mind, here are five signs it might be time for you to refinance:

- It’s been at least two years since you took out your loan. Credit policies, interest rates and borrower incentives have changed a lot in that time, so you might find that better loan options are now available.

- Your financial situation is now different. Just as you need new clothes when your body changes, you generally need a new loan when your personal circumstances evolve.

- Your fixed-rate period is coming to an end. Instead of reverting to your lender’s standard variable rate, look around to see if better loan options are available – because the answer will probably be yes.

- You’ve built up equity in your property. If your equity position is stronger, you might now be able to qualify for a loan with a lower interest rate or better features.

You want to cash out equity. If you want to buy an investment property, you might be able to cash out equity – via a refinance – and use that money to fund the deposit.